Research Archives

Sovereign

Intelligence

Public research archives — browse dossiers without signing in

SEC Narrative Culmination // OSCR

for Oscar Health, Inc. (OSCR) at $26.54. --- Strategic Thesis: Oscar Health, Inc. (OSCR) **Price:** $26.54 | **Date:** 2026-08-07 **Recommendation:** **HOLD / ACCUMULATE (Spec...

SEC Narrative Culmination // OSCR

Based on the extracted intelligence from the 10-Q filing for the period ending June 30, 2026 (filed 2026-08-07), here is the Strategic Thesis for Oscar Health, Inc. (OSCR) at $26.54.

---

Strategic Thesis: Oscar Health, Inc. (OSCR)

Price: $26.54 | Date: 2026-08-07

Recommendation: HOLD / ACCUMULATE (Speculative)

---

1. Core Narrative (The "What")

Oscar Health is evolving from a high-growth insurtech into a mature, capital-dense health insurer that is transitioning from a model reliant on external funding to one that can self-sustain through subsidiary profitability and statutory surplus. The strategy hinges on leveraging significant investment income (yield) to offset underwriting pressure and aggressively managing regulatory risk (CMS clawbacks). The future of the stock is now tied to profitability efficiency and capital returns, not just premium growth.

2. Strategic Drivers & Inflection Points

- The "Yield" Bridge: The most significant strategic shift visible in the data is the explosion in investing activities. Net cash used in investing activities surged to $3,42 billion for H1 2026 versus $342 million in H1 2025 (a ~10x increase). This suggests the company is building a massive fixed-income/short-term investment portfolio. The thesis hinges on: Can they earn a higher yield on this portfolio than the cost of claims and administration? This is the primary profit engine for 2026.

- The "Tariff & Cost" Headwind: The filing explicitly calls out new Trump administration tariffs on pharmaceutical products. This is a direct threat to Medical Loss Ratio (MLR). Their ability to negotiate with pharmacy benefit managers (PBMs) and providers to pass through or absorb these costs will be a key differentiator.

- The "Cigna" Aftermath: The company explicitly confirms it did not renew the Cigna+Oscar Small Group arrangement (expired 12/31/2024). The market share loss is now a sunk cost; the question is whether the fully internalized member base is profitable and sticky enough to offset this lost revenue.

- Liquidity & Capital Management: The balance sheet shows significant cash flow volatility (large cash disbursements, high investment purchases). The ability to make dividends upstream from profitable health subsidiaries is explicitly mentioned. This suggests the company is entering a phase of "capital release" rather than "capital raising."

3. Financial Data Points (Distilled)

- Investing Strategy: Massive scale-up in investment purchases (Short-term investments ~$4.48bn; Total assets ~$6.27bn). This is a "risk-off" portfolio (US Treasury/agency heavy) aimed at generating net investment income.

- Cash Flow Stretch: Operating cash flows are being squeezed by higher claim disbursements offset only by higher premiums received. The company is running a capital-intensive model.

- Debt Load: The company has convertible debt. Coupon interest expense is $5.88 million for Q2 2026 and $11.05 million for H1 2026. While not high in absolute terms, this is a fixed cost against variable claim risk.

4. Identified Risks & Red Flags

- Credit Risk (Counterparty): The filing details an allowance for credit losses on receivables. There is inherent risk that some receivables (likely from CMS or providers) become uncollectible, impacting cash flow.

- Regulatory Sanctions: The company explicitly states it remains subject to reviews which "could result in additional fines or other sanctions." This indicates ongoing regulatory friction is a recurring operational risk.

- Interest Rate Sensitivity: While they are buying bonds for yield, an unexpected rate-cut cycle would compress their investment income margin, while claim costs (healthcare) remain inflationary.

- Morbidity Misestimation: The risk of underestimating market morbidity remains the #1 existential threat. If they underpriced 2026 premiums, the "yield bridge" will not be enough to cover the losses.

5. Market Positioning & Competitive Landscape

- Niche Player: Oscar remains a smaller player relative to UnitedHealth or Elevance. They aim to compete on user experience (tech) and specific market selection (e.g., Texas, Florida) where they can price rationally.

- The "Insurance as a Utility" Model: They are optimizing for cash flow and statutory surplus, not just top-line membership growth. This is a defensive posture, suggesting a mature market where they are prioritizing survival/consolidation over expansion.

---

Strategic Decision Matrix for OSCR

| Factor | Current Status (2026-08-07) | Strategic Implication for Investors |

| -------------------- | ------------------------------------------------------------------------------------------- | ---------------------------------------------------------------------------------------------------- |

| Capital Allocation | Massive shift to investment income generation ($3.4B in purchases). | Positive (Earnings Replacement). The company is replacing volatile premium growth with stable yield. |

| Operational Risk | Tariffs on pharma + MLR uncertainty. | Negative (Margin Compression). Management must execute on cost controls to maintain profitability. |

| Financial Health | Large asset base ($6.27B), but high cash outflows and interest expense. | Neutral. They have a cushion, but the liquidity strain is a watch item. |

| Growth Strategy | Defensive—no longer relying on the Cigna partnership; focusing on organic profitability. | Contrarian Positive. If they post a profitable 2026, the stock re-rates as a "cash cow" rather than a growth story. |

---

Conclusion: How to Play It

At $26.54, the market is pricing in a stable but not explosive future.

- The Bull Case: The company successfully navigates tariff costs, investment income covers claims variability, and the company announces its first major statutory dividend upstream to the holdco. This would push the stock towards $32-$35.

- The Bear Case: Investment income is wiped out by a 1-2% MLR deterioration, or CMS audits force significant premium refunds, crushing liquidity.

Verdict: This is a "Show Me" stock. The strategy is sound (yield generation to smooth earnings), but the execution risk is high. Accumulate on weakness below $25.00 if you believe the yield bridge holds. Avoid chasing momentum above $28 without clear evidence of MLR stability.

---

Disclaimer: This analysis is based solely on the provided file extraction and the "Vigintagon" framework. It does not constitute financial advice. Please consult a licensed advisor who can review the full 10-Q.

SEC Narrative Culmination // CELH

Based on the provided information, here is a ruthless strategic thesis for Celsius Holdings, Inc. (CELH): **Thesis:** Celsius Holdings, Inc. (CELH) is a high-growth company in the...

SEC Narrative Culmination // CELH

Based on the provided information, here is a ruthless strategic thesis for Celsius Holdings, Inc. (CELH):

Thesis: Celsius Holdings, Inc. (CELH) is a high-growth company in the functional energy drink market, with a strong brand portfolio and expanding distribution network. However, the company faces significant risks and challenges, including intense competition, regulatory scrutiny, and potential disruptions to its supply chain and distribution network.

Key Strengths:

1. Strong brand portfolio: CELH has a diverse portfolio of brands, including CELSIUS, Alani Nu, and Rockstar, which cater to different consumer preferences and demographics.

2. Expanding distribution network: The company has a growing distribution network, with partnerships with major retailers and distributors, including PepsiCo.

3. Innovative products: CELH has a strong track record of innovation, with new product launches and line extensions that cater to changing consumer preferences.

Key Weaknesses:

1. Intense competition: The functional energy drink market is highly competitive, with established players like Red Bull, Monster, and Rockstar, as well as new entrants and private label brands.

2. Regulatory scrutiny: The company faces regulatory risks, including potential changes to labeling and marketing regulations, as well as scrutiny over the use of certain ingredients.

3. Supply chain and distribution risks: CELH relies on third-party manufacturers and distributors, which can be subject to disruptions and delays.

Key Opportunities:

1. Growing demand for functional beverages: The demand for functional beverages, including energy drinks, is growing, driven by consumer interest in health and wellness.

2. Expanding distribution channels: The company can expand its distribution channels, including e-commerce, convenience stores, and foodservice outlets.

3. Innovation and new product development: CELH can continue to innovate and launch new products that cater to changing consumer preferences and trends.

Key Threats:

1. Competition from established players: Established players in the energy drink market, such as Red Bull and Monster, may respond to CELH's growth by increasing their marketing and promotional efforts.

2. Regulatory changes: Changes to labeling and marketing regulations, as well as potential bans on certain ingredients, could negatively impact CELH's business.

3. Supply chain disruptions: Disruptions to CELH's supply chain, including manufacturing and distribution delays, could impact the company's ability to meet demand and maintain its growth trajectory.

Investment Thesis: Based on the analysis above, an investment in CELH could be attractive for investors who are willing to take on the risks associated with a high-growth company in a competitive market. The company's strong brand portfolio, expanding distribution network, and innovative products position it for continued growth, but investors should be aware of the potential risks and challenges that the company faces.

Ruthless Strategic Recommendations:

1. Focus on innovation and new product development: CELH should continue to invest in innovation and new product development to stay ahead of the competition and cater to changing consumer preferences.

2. Expand distribution channels: The company should expand its distribution channels, including e-commerce, convenience stores, and foodservice outlets, to increase its reach and availability.

3. Diversify supply chain and distribution network: CELH should diversify its supply chain and distribution network to reduce its reliance on third-party manufacturers and distributors and mitigate the risk of disruptions.

4. Invest in marketing and advertising: The company should invest in marketing and advertising to increase brand awareness and drive sales, particularly in new and emerging markets.

5. Monitor regulatory developments: CELH should closely monitor regulatory developments and engage with regulators to ensure that its products and marketing practices comply with changing regulations and standards.

SEC Narrative Culmination // VITL

:** Vital Farms, Inc. (VITL) is a high-growth company in the specialty egg and dairy market, with a strong brand and increasing market share. However, the company faces significan...

SEC Narrative Culmination // VITL

Ruthless Strategic Thesis:

Vital Farms, Inc. (VITL) is a high-growth company in the specialty egg and dairy market, with a strong brand and increasing market share. However, the company faces significant risks and challenges, including intense competition, supply chain disruptions, and regulatory risks.

Key Strengths:

1. Strong brand: Vital Farms has a well-established brand with a loyal customer base, which provides a competitive advantage in the market.

2. Increasing market share: The company has been gaining market share in the specialty egg and dairy market, driven by its focus on high-quality products and sustainable farming practices.

3. Diversified product portfolio: Vital Farms offers a range of products, including eggs, butter, and hard-boiled eggs, which helps to reduce dependence on a single product and increases revenue streams.

Key Weaknesses:

1. Intense competition: The specialty egg and dairy market is highly competitive, with many established players and new entrants, which could lead to pricing pressure and reduced market share.

2. Supply chain disruptions: Vital Farms relies on a network of family farms and suppliers, which can be vulnerable to disruptions, such as disease outbreaks, weather events, and trade policies.

3. Regulatory risks: The company is subject to various regulations, including food safety and environmental regulations, which can be complex and costly to comply with.

Key Opportunities:

1. Growing demand for specialty eggs and dairy: The market for specialty eggs and dairy products is growing, driven by increasing consumer demand for high-quality, sustainable, and healthy products.

2. Expansion into new markets: Vital Farms can expand its product offerings and distribution channels into new markets, such as foodservice and international markets.

3. Innovation and product development: The company can invest in research and development to create new and innovative products, which can help to drive growth and increase market share.

Key Threats:

1. Competition from larger players: Larger players in the market, such as conventional egg and dairy companies, may enter the specialty market, which could lead to increased competition and pricing pressure.

2. Supply chain disruptions: Disruptions to the supply chain, such as disease outbreaks or trade policies, can impact the company's ability to produce and distribute products.

3. Regulatory changes: Changes to regulations, such as food safety and environmental regulations, can increase costs and complexity for the company.

Investment Thesis:

Based on the analysis, Vital Farms, Inc. (VITL) is a high-growth company with a strong brand and increasing market share. However, the company faces significant risks and challenges, including intense competition, supply chain disruptions, and regulatory risks. To mitigate these risks, the company should focus on:

1. Diversifying its supply chain: Vital Farms should diversify its supply chain to reduce dependence on a single supplier or region.

2. Investing in innovation and product development: The company should invest in research and development to create new and innovative products, which can help to drive growth and increase market share.

3. Expanding into new markets: Vital Farms should expand its product offerings and distribution channels into new markets, such as foodservice and international markets.

Overall, Vital Farms, Inc. (VITL) is a high-growth company with significant potential, but it requires careful management of risks and challenges to achieve long-term success.

SEC Narrative Culmination // JOBY

Based on the provided information, here is a ruthless strategic thesis for Joby Aviation: **Thesis:** Joby Aviation is a high-risk, high-reward investment opportunity in the emerg...

SEC Narrative Culmination // JOBY

Based on the provided information, here is a ruthless strategic thesis for Joby Aviation:

Thesis: Joby Aviation is a high-risk, high-reward investment opportunity in the emerging urban air mobility (UAM) market. The company's vertically integrated business model, proprietary technology, and strategic partnerships position it for potential success, but significant challenges and uncertainties remain.

Key Strengths:

1. First-mover advantage: Joby Aviation is one of the pioneers in the UAM market, with a head start in developing and certifying its eVTOL aircraft.

2. Vertically integrated business model: The company's control over design, manufacturing, and operations enables it to optimize performance, safety, and customer experience.

3. Strategic partnerships: Collaborations with major players like Toyota, Uber, and Delta Air Lines provide access to resources, expertise, and market opportunities.

4. Proprietary technology: Joby Aviation's eVTOL aircraft and operating system are designed to provide a unique and efficient solution for UAM.

Key Weaknesses:

1. Regulatory uncertainty: The UAM market is still in its infancy, and regulatory frameworks are evolving. Delays or changes in certification processes could significantly impact Joby Aviation's timelines and costs.

2. Competition: The UAM market is attracting numerous entrants, including established aerospace companies and new startups. Intense competition could lead to pricing pressure, reduced market share, and increased marketing expenses.

3. Technical risks: The development and certification of eVTOL aircraft are complex and challenging. Technical issues, accidents, or certification delays could damage the company's reputation and financials.

4. Capital requirements: Joby Aviation will require significant funding to scale its operations, develop infrastructure, and achieve profitability. Access to capital and financing terms may be uncertain.

Key Opportunities:

1. Growing demand: The UAM market is expected to experience rapid growth, driven by increasing urbanization, traffic congestion, and environmental concerns.

2. Expanding services: Joby Aviation can leverage its technology and infrastructure to offer a range of services, including passenger transportation, cargo delivery, and medical emergency services.

3. Strategic acquisitions: The company can consider acquiring complementary technologies, businesses, or assets to enhance its capabilities and market position.

4. International expansion: Joby Aviation can explore opportunities in international markets, leveraging its partnerships and expertise to navigate local regulatory environments and customer needs.

Key Threats:

1. Regulatory changes: Changes in regulatory frameworks, safety standards, or environmental policies could increase costs, delay certification, or limit market access.

2. Competition from established players: Incumbent aerospace companies and new entrants may leverage their resources, expertise, and brand recognition to challenge Joby Aviation's market position.

3. Technical disruptions: Advances in alternative technologies, such as autonomous ground vehicles or hyperloop systems, could potentially disrupt the UAM market and reduce demand for eVTOL aircraft.

4. Economic downturn: An economic recession or downturn could reduce demand for UAM services, limit access to capital, and increase financing costs.

Investment Strategy:

1. Monitor regulatory developments: Closely follow updates on regulatory frameworks, certification processes, and safety standards to assess their impact on Joby Aviation's timelines and costs.

2. Track competition: Continuously monitor the competitive landscape, including new entrants, partnerships, and technological advancements, to assess Joby Aviation's market position and potential threats.

3. Assess technical progress: Evaluate the company's technical milestones, certification progress, and operational performance to gauge its ability to execute on its business plan.

4. Evaluate financing options: Consider Joby Aviation's access to capital, financing terms, and cash burn rate to determine its ability to scale operations and achieve profitability.

By carefully weighing these factors and continuously monitoring the company's progress, investors can make an informed decision about the potential risks and rewards of investing in Joby Aviation.

SEC Narrative Culmination // UUUU

:** Energy Fuels Inc. (UUUU) is a critical materials company with a diversified portfolio of uranium, vanadium, rare earth elements (REEs), and heavy mineral sands (HMS) assets. T...

SEC Narrative Culmination // UUUU

Ruthless Strategic Thesis:

Energy Fuels Inc. (UUUU) is a critical materials company with a diversified portfolio of uranium, vanadium, rare earth elements (REEs), and heavy mineral sands (HMS) assets. The company's strategic position in the global market, combined with its operational flexibility and growth potential, presents a compelling investment opportunity.

Key Investment Highlights:

1. Uranium Market Trends: The uranium market is experiencing a resurgence, driven by growing demand for clean energy and nuclear power. Energy Fuels is well-positioned to capitalize on this trend, with a strong portfolio of uranium assets and a proven track record of production.

2. REE Market Growth: The REE market is expected to experience significant growth, driven by increasing demand for advanced technologies, such as electric vehicles, wind turbines, and robotics. Energy Fuels' REE initiatives, including its monazite processing capabilities and joint venture interests, position the company for success in this market.

3. HMS Segment: The HMS segment, which includes ilmenite, rutile, and zircon production, provides a stable source of revenue and cash flow for the company.

4. Operational Flexibility: Energy Fuels' White Mesa Mill, located in Utah, is a critical asset that provides operational flexibility and allows the company to process a variety of feedstocks, including uranium, vanadium, and REEs.

5. Growth Potential: The company has a strong pipeline of growth projects, including the Vara Mada Project, the Donald Project, and the Roca Honda Project, which are expected to drive future production and revenue growth.

Risks and Challenges:

1. Commodity Price Volatility: Energy Fuels' revenue and profitability are exposed to commodity price volatility, particularly in the uranium and REE markets.

2. Regulatory Risks: The company is subject to various regulatory risks, including changes in environmental and safety regulations, which can impact operations and profitability.

3. Competition: The uranium, REE, and HMS markets are highly competitive, and Energy Fuels faces competition from established players and new entrants.

Investment Strategy:

1. Long-Term Focus: Invest in Energy Fuels with a long-term focus, as the company's growth potential and strategic position in the market are expected to drive value creation over time.

2. Diversification: Consider diversifying your portfolio by investing in a range of critical materials companies, including those with exposure to uranium, REEs, and HMS.

3. Active Management: Monitor the company's progress and adjust your investment strategy as needed to respond to changes in the market and the company's operations.

Target Price:

Based on the company's growth potential, strategic position, and operational flexibility, we establish a target price of $25.00 per share, representing a 49% upside from the current market price of $16.78.

SEC Narrative Culmination // ROOT

:** Root, Inc. (ROOT) is a technology company operating in the insurance industry, primarily offering auto and renters insurance products through a direct-to-consumer model. The c...

SEC Narrative Culmination // ROOT

Ruthless Strategic Thesis:

Root, Inc. (ROOT) is a technology company operating in the insurance industry, primarily offering auto and renters insurance products through a direct-to-consumer model. The company has demonstrated growth in its partnership channel and has reduced its reliance on quota share reinsurance. However, the insurance industry is highly competitive, and Root faces challenges in maintaining profitability due to increasing loss costs and expenses.

Key Observations:

1. Gross Premiums Written: Decreased by 5.3% in the three months ended March 31, 2026, primarily due to a decline in new writings in the direct channel.

2. Net Premiums Earned: Increased by 13.2% in the three months ended March 31, 2026, driven by a reduction in cessions of gross premiums earned to reinsurers.

3. Loss and Loss Adjustment Expenses (LAE): Increased by 10.0% in the three months ended March 31, 2026, due to higher loss costs and reduced cessions of losses to reinsurers.

4. Sales and Marketing Expenses: Decreased by 47.0% in the three months ended March 31, 2026, reflecting a reduction in direct performance marketing spend.

5. Other Insurance Expense: Increased by 61.9% in the three months ended March 31, 2026, primarily due to higher acquisition expenses and amortization of deferred policy acquisition costs.

Strategic Recommendations:

1. Optimize Pricing Strategy: Root should focus on optimizing its pricing strategy to balance growth with profitability, considering factors like loss costs, competition, and customer demand.

2. Enhance Risk Management: The company should continue to invest in risk management capabilities, including data analytics and modeling, to better assess and manage risk.

3. Diversify Distribution Channels: Root should explore alternative distribution channels, such as partnerships with other insurers or fintech companies, to reduce dependence on its direct channel.

4. Invest in Technology: The company should continue to invest in technology, including artificial intelligence and machine learning, to improve underwriting, claims processing, and customer engagement.

5. Monitor Regulatory Environment: Root should closely monitor the regulatory environment and adapt to changes in laws and regulations that may impact its business.

Investment Thesis:

Based on the analysis, Root, Inc. (ROOT) is a speculative investment opportunity, given its growth potential and innovative approach to the insurance industry. However, the company's profitability and competitiveness are uncertain, and investors should carefully consider the risks and challenges associated with the insurance industry.

Target Price: $60.00

Investment Horizon: 12-18 months

Risk Tolerance: High

This strategic thesis is based on the provided document and may not reflect the current market situation or the company's latest developments. Investors should conduct their own research and consider multiple sources before making any investment decisions.

SEC Narrative Culmination // MSTR

Based on the provided SEC filing excerpt, here is a ruthless strategic thesis for Strategy Inc (MSTR): **Thesis:** Strategy Inc's bitcoin-centric business model, while innovative,...

SEC Narrative Culmination // MSTR

Based on the provided SEC filing excerpt, here is a ruthless strategic thesis for Strategy Inc (MSTR):

Thesis: Strategy Inc's bitcoin-centric business model, while innovative, poses significant risks due to the volatility of bitcoin prices, regulatory uncertainty, and potential liquidity issues. The company's reliance on debt financing and convertible notes adds to the complexity of its financial structure. Despite these challenges, the company's commitment to its bitcoin strategy and its ability to adapt to changing market conditions could potentially lead to long-term growth and increased shareholder value.

Key Points:

1. Bitcoin Price Volatility: The company's financial performance is heavily influenced by the price of bitcoin, which can be highly volatile.

2. Regulatory Uncertainty: The regulatory environment for digital assets is evolving, and changes in laws or regulations could negatively impact the company's business.

3. Liquidity Risks: The company's reliance on debt financing and convertible notes poses liquidity risks, particularly if the price of bitcoin declines significantly.

4. Complex Financial Structure: The company's use of convertible notes and preferred stock adds complexity to its financial structure, which can make it challenging for investors to understand the company's financial performance.

5. Adaptability: Despite the challenges, the company has demonstrated its ability to adapt to changing market conditions, which could potentially lead to long-term growth and increased shareholder value.

Investment Strategy:

1. Long-term Focus: Investors should take a long-term view when investing in Strategy Inc, as the company's financial performance can be volatile in the short term.

2. Diversification: Investors should consider diversifying their portfolio to mitigate the risks associated with investing in a single company with a bitcoin-centric business model.

3. Monitoring Regulatory Developments: Investors should closely monitor regulatory developments and changes in laws or regulations that could impact the company's business.

4. Financial Discipline: The company should maintain financial discipline and avoid taking on excessive debt or engaging in risky financial transactions.

5. Innovation: The company should continue to innovate and adapt to changing market conditions to remain competitive and drive long-term growth.

Conclusion:

Strategy Inc's bitcoin-centric business model poses significant risks, but the company's commitment to its strategy and its ability to adapt to changing market conditions could potentially lead to long-term growth and increased shareholder value. Investors should take a long-term view, diversify their portfolio, and closely monitor regulatory developments to mitigate the risks associated with investing in this company.

SEC Narrative Culmination // BMNR

: The "Phoenix" Transition from Mining Operator to Digital Asset Financial Engineer **Core Thesis:** Bitmine Immersion Technologies is executing a fundamental strategic pivot, tra...

SEC Narrative Culmination // BMNR

Based on the provided filing intelligence for Bitmine Immersion Technologies, Inc. (BMNR), here is the strategic thesis.

Strategic Thesis: The "Phoenix" Transition from Mining Operator to Digital Asset Financial Engineer

Core Thesis: Bitmine Immersion Technologies is executing a fundamental strategic pivot, transitioning from a capital-intensive, operationally-heavy Bitcoin mining and hosting company to a leaner, financial-engineering-focused entity. The company is actively winding down its legacy mining and hosting operations to shed unprofitable business lines, reduce operational risk, and restructure its capital base. The new strategy leverages its remaining infrastructure, industry expertise, and financial instruments (leases, options, structured settlements) to generate revenue and manage its substantial debt and equity overhang, with the ultimate goal of achieving a sustainable, less volatile business model geared toward surviving the next crypto cycle.

---

Strategic Rationale & Key Strategic Vectors

#### 1. The "Legacy" Disposal & Risk Mitigation (The "Winding Down"):

The filings explicitly state the company is "winding down its proprietary self-mining exposure and deferring new site buildouts." This is a critical strategic admission. The legacy business (hosting, self-mining, equipment sales) was characterized by:

- High Operational Leverage & Volatility: Revenue was directly tied to the volatile price of Bitcoin, unpredictable hardware costs, and intense competition for hosting clients.

- Unsustainable CapEx: Building and operating hosting centers required massive capital outlay, which the company's financials (persistent losses from operations, debt extinguishment losses) show it could not sustain.

- Balance Sheet Distress: The filings reveal a complex web of debt, convertible notes, preferred shares, and warrant liabilities. The company is actively managing this overhang through conversions, settlements (like the letter agreement with Jonathan Bates and IDI), and debt restructurings.

Strategic Vector: The company is sacrificing top-line revenue potential to eliminate the cash-burning and balance-sheet-destroying aspects of its legacy operations. This is a survival move, not a growth move.

#### 2. The Emergence of the "Financial Engineer" (The "Rise"):

The new strategy, while nascent, is visible through the remaining business activities:

- Strategic Leasing (The KULR Deal): The filing mentions a machine lease agreement with KULR Technology Group. This represents a shift from selling hash rate or providing hosting services to leasing capital assets. This is a less capital-intensive, more predictable revenue stream than self-mining.

- Derivative & Options Trading: The presence of "ETH option contracts" and "option premium income" is the most telling sign of the new strategy. The company is actively using financial derivatives on digital assets, treating its balance sheet and market knowledge as a trading desk.

- Debt Restructuring as a Core Competency: The filings are replete with examples of converting debt, settling preferred shares, and renegotiating payment terms. The company is effectively using its own distressed capital structure as a tool for survival, buying time and reducing absolute liability.

- De-emphasis of Self-Mining: The "wind down" of self-mining is a clear abandonment of the core value proposition of a traditional mining company. The new thesis is not about being the lowest-cost miner, but about being a nimble asset manager in the digital asset space.

Strategic Vector: The company is attempting to morph into a hybrid entity: part equipment lessor, part options trader, and part distressed-debt workout specialist. The goal is to generate non-mining revenue and manage its balance sheet towards a net-positive equity position.

#### 3. Key Risks & Execution Challenges (The "Threats"):

- Liquidity & Survival Risk: The financials show persistent losses from operations and a very complex capital structure. The success of the pivot hinges entirely on staying solvent long enough for the new financial engineering strategies to generate material, positive cash flow.

- Dependence on Bitcoin/ETH Price: While the company is reducing direct mining exposure, its derivative and leasing activities are still correlated to the price and volatility of digital assets. A prolonged "crypto winter" would severely stress the new model.

- Execution Risk on Financial Engineering: The company's foray into options trading and complex derivatives is a high-risk, high-reward activity for a company with limited resources. A single bad trade could be catastrophic. This is a fragile, capital-restrained trader, not a well-funded hedge fund.

- Regulatory Scrutiny: The filings explicitly mention regulatory risks for digital asset holdings and custody. As the company engages in more financial activities (options, staking, potential tokenization), it will face increased regulatory attention.

- Shareholder Dilution: The constant stream of debt and preferred share conversions into common stock will continue to dilute existing shareholders, pressuring the stock price.

Strategic Outlook for BMNR ($19.39)

The company is in a "show me" phase. The legacy mining business is dying, and the new financial engineering business is not yet proven to be profitable or sustainable. The current stock price likely reflects a combination of:

1. Speculation on the Bitcoin/ETH recovery: Investors hoping the pivot works if the market rallies.

2. A "distressed asset" valuation: The price may simply reflect the complex liquidation or restructuring value of the remaining assets (leased miners, cash, digital asset holdings).

3. A belief in the financial engineering team: That the management's ability to restructure debt and generate premium income (from options) will ultimately create shareholder value.

Successful execution of the strategic thesis requires:

- Proving the derivative/options strategy is consistently profitable over a rolling period.

- Generating positive adjusted operating income as shown in the non-GAAP metrics, removing the non-cash losses from warrant liabilities and digital asset impairments.

- Stabilizing the balance sheet by significantly reducing total debt and the dilution from future conversions.

Risk of failure:

- A market downturn that makes the derivative strategy unprofitable.

- A failure to secure a major new lease or equivalent capital-light revenue stream.

- A dilutive event (e.g., a forced equity raise) that destroys further shareholder value.

Conclusion: BMNR is a high-risk, speculative "turnaround" story. It is not a traditional Bitcoin mining company. It is a micro-cap company attempting a complex transformation into a digital asset financial boutique. For the thesis to be validated, the company must demonstrate that its new, less asset-intensive, more financial-engineered model can generate positive cash flow and de-risk its balance sheet, moving it from a state of "managed decline" to "controlled regeneration." The stock price is a wager on the management's ability to execute this high-wire act.

SEC Narrative Culmination // NAVN

Based on the provided SEC filing excerpts, here is a ruthless strategic thesis for Navan, Inc. (NAVN): **Investment Thesis:** Navan, Inc. (NAVN) is a cloud-based technology platf...

SEC Narrative Culmination // NAVN

Based on the provided SEC filing excerpts, here is a ruthless strategic thesis for Navan, Inc. (NAVN):

Investment Thesis:

Navan, Inc. (NAVN) is a cloud-based technology platform providing travel, payments, and expense management solutions to businesses. Despite its rapid growth and increasing revenue, the company faces significant challenges, including intense competition, high operating expenses, and dependence on third-party vendors. The recent IPO has provided a cash infusion, but the company's ability to achieve profitability and sustain growth is uncertain.

Key Risks:

1. Competition: The travel and expense management market is highly competitive, with established players and new entrants leveraging AI and automation.

2. Operating Expenses: Navan's operating expenses are high, particularly in sales and marketing, and may continue to increase as the company expands.

3. Third-Party Dependence: The company relies on third-party vendors for critical services, including payment processing and travel bookings, which poses risks to its operations and revenue.

4. Regulatory Risks: Navan is subject to various regulations, including those related to payments, data privacy, and anti-money laundering, which can be complex and costly to comply with.

5. Macroeconomic Risks: The company's revenue is sensitive to macroeconomic conditions, including economic downturns, geopolitical events, and changes in business travel demand.

Opportunities:

1. Growing Demand: The demand for digital travel and expense management solutions is increasing, driven by the shift to remote work and the need for more efficient and automated processes.

2. Expansion into New Markets: Navan has opportunities to expand into new markets, including international markets and industries with high travel and expense management needs.

3. AI and Automation: The company's investment in AI and automation can help improve its platform's efficiency, reduce costs, and enhance the user experience.

4. Strategic Partnerships: Navan can form strategic partnerships with other companies to expand its offerings and reach new customers.

Valuation:

Based on the provided excerpts, Navan's valuation is not explicitly stated. However, considering the company's growth rate, revenue, and operating expenses, a reasonable valuation multiple could be applied to estimate its value.

Recommendation:

Given the risks and opportunities outlined above, a ruthless strategic thesis for Navan, Inc. (NAVN) could be:

Short Navan, Inc. (NAVN)

The company's high operating expenses, intense competition, and dependence on third-party vendors pose significant risks to its ability to achieve profitability and sustain growth. While the demand for digital travel and expense management solutions is growing, Navan's valuation may be overstated, and the company's ability to execute on its growth strategy is uncertain. A short position in Navan, Inc. (NAVN) could be a profitable trade, especially if the company fails to meet its growth expectations or experiences significant disruptions to its operations.

Disclaimer:

This analysis is based on the provided SEC filing excerpts and should not be considered as investment advice. The views expressed are those of a ruthless strategic analyst and may not reflect the opinions of others. It is essential to conduct thorough research and consult with financial experts before making any investment decisions.

SEC Narrative Culmination // UEC

:** Based on the provided document, Uranium Energy Corp (UEC) is a fast-growing, uranium mining company with a focus on becoming a leading low-cost North American uranium supplier...

SEC Narrative Culmination // UEC

Ruthless Strategic Thesis:

Based on the provided document, Uranium Energy Corp (UEC) is a fast-growing, uranium mining company with a focus on becoming a leading low-cost North American uranium supplier. The company has a strong portfolio of projects, including the Christensen Ranch Mine, Burke Hollow Project, and Roughrider Project, among others.

Key Strengths:

1. Diversified Project Portfolio: UEC has a diverse range of projects in various stages of development, providing a solid foundation for future growth.

2. Low-Cost Production: The company's focus on in-situ recovery (ISR) mining and its strategic location in North America position it for low-cost production.

3. Strong Management Team: UEC's management team has extensive experience in the uranium industry, which is crucial for navigating the complex regulatory and operational landscape.

Key Weaknesses:

1. Dependence on Uranium Prices: UEC's revenue and profitability are heavily dependent on uranium prices, which can be volatile and subject to market fluctuations.

2. Regulatory Risks: The company is subject to various regulatory requirements and risks, including environmental and safety regulations, which can impact its operations and profitability.

3. Competition: The uranium industry is highly competitive, with several established players, which can make it challenging for UEC to differentiate itself and achieve market share.

Opportunities:

1. Growing Demand for Uranium: The increasing demand for clean energy and the growing recognition of nuclear power as a viable source of electricity are expected to drive demand for uranium.

2. Expansion into New Markets: UEC can explore opportunities to expand into new markets, such as Asia, where nuclear power is becoming increasingly important.

3. Strategic Acquisitions: The company can consider strategic acquisitions to enhance its project portfolio, increase its market share, and improve its competitive position.

Threats:

1. Market Volatility: Uranium prices can be highly volatile, which can impact UEC's revenue and profitability.

2. Regulatory Changes: Changes in regulatory requirements or policies can affect the company's operations and profitability.

3. Competition from Alternative Energy Sources: The growing adoption of alternative energy sources, such as solar and wind power, can potentially reduce demand for uranium and impact UEC's business.

Strategic Recommendations:

1. Diversify Revenue Streams: UEC should consider diversifying its revenue streams by exploring opportunities in other markets, such as nuclear fuel services or uranium trading.

2. Invest in Technology: The company should invest in technology to improve its operational efficiency, reduce costs, and enhance its competitive position.

3. Strengthen Partnerships: UEC should focus on building strong partnerships with key stakeholders, including suppliers, customers, and regulatory bodies, to ensure a stable and supportive business environment.

Investment Thesis:

UEC is a promising company with a strong portfolio of projects and a solid management team. While the company faces challenges, including regulatory risks and market volatility, its strategic position and growth potential make it an attractive investment opportunity. With a focus on diversifying revenue streams, investing in technology, and strengthening partnerships, UEC can navigate the challenges and capitalize on the opportunities in the uranium industry.

Target Price: $15.50

Investment Horizon: 12-18 months

Risk Tolerance: Medium to High

This ruthless strategic thesis provides a comprehensive analysis of UEC's strengths, weaknesses, opportunities, and threats, and offers strategic recommendations to enhance the company's competitive position and drive growth. The investment thesis provides a clear investment case, including a target price, investment horizon, and risk tolerance, to help investors make informed decisions.

SEC Narrative Culmination // OMDA

:** To drive growth and increase profitability, Omada should focus on the following strategies: 1. **Diversify Customer Base:** Reduce dependence on a limited number of customers ...

SEC Narrative Culmination // OMDA

Based on the provided text, I will analyze the data and provide a ruthless strategic thesis.

Company Overview:

Omada Health, Inc. (OMDA) is a virtual care company that offers various programs for chronic condition management, including diabetes, hypertension, and musculoskeletal (MSK) conditions. The company has experienced rapid growth, with revenue increasing by 53% in 2025 compared to 2024.

Key Strengths:

1. Growing Demand: The demand for virtual care services is increasing, driven by the growing prevalence of chronic conditions and the need for convenient, cost-effective healthcare solutions.

2. Diversified Program Offerings: Omada offers a range of programs, including diabetes, hypertension, and MSK conditions, which helps to reduce dependence on a single program and increases the company's appeal to a broader customer base.

3. Strong Customer Relationships: Omada has established relationships with major health plans and employers, which provides a stable source of revenue and helps to drive growth.

Key Weaknesses:

1. Dependence on Customer Concentration: A significant portion of Omada's revenue comes from a limited number of customers, which increases the risk of revenue volatility if one or more of these customers were to terminate their contracts.

2. High Customer Acquisition Costs: Omada incurs significant costs to acquire new customers, which can be a barrier to growth and profitability.

3. Regulatory Risks: The virtual care industry is subject to various regulatory risks, including changes in reimbursement policies and potential scrutiny from regulatory bodies.

Key Opportunities:

1. Expanding into New Markets: Omada can expand its services into new markets, including international markets, to drive growth and increase revenue.

2. Developing New Programs: The company can develop new programs to address emerging healthcare needs, such as mental health and wellness, to increase its offerings and appeal to a broader customer base.

3. Strategic Partnerships: Omada can form strategic partnerships with healthcare providers, payers, and technology companies to increase its reach and offerings.

Key Threats:

1. Competition: The virtual care industry is highly competitive, with many established players and new entrants, which can make it challenging for Omada to differentiate itself and maintain market share.

2. Regulatory Changes: Changes in regulatory policies, such as reimbursement rates or certification requirements, can negatively impact Omada's business and revenue.

3. Economic Downturn: An economic downturn can reduce demand for virtual care services, which can negatively impact Omada's revenue and growth.

Ruthless Strategic Thesis:

To drive growth and increase profitability, Omada should focus on the following strategies:

1. Diversify Customer Base: Reduce dependence on a limited number of customers by expanding into new markets and developing new programs.

2. Invest in Digital Transformation: Invest in digital technologies, such as AI and machine learning, to enhance the customer experience, improve outcomes, and reduce costs.

3. Develop Strategic Partnerships: Form partnerships with healthcare providers, payers, and technology companies to increase reach and offerings.

4. Focus on High-Growth Markets: Focus on high-growth markets, such as international markets, to drive revenue and expansion.

5. Optimize Operations: Optimize operations to reduce costs and improve efficiency, which can help to increase profitability and competitiveness.

By executing these strategies, Omada can drive growth, increase profitability, and establish itself as a leader in the virtual care industry.

SEC Narrative Culmination // INFQ

Based on the provided SEC filing excerpts, here is a ruthless strategic thesis for Infleqtion, Inc. (INFQ): **Investment Thesis:** Infleqtion, Inc. (INFQ) is a high-risk, high-re...

SEC Narrative Culmination // INFQ

Based on the provided SEC filing excerpts, here is a ruthless strategic thesis for Infleqtion, Inc. (INFQ):

Investment Thesis:

Infleqtion, Inc. (INFQ) is a high-risk, high-reward investment opportunity in the emerging quantum technology industry. The company has completed a business combination with ColdQuanta, Inc. and has a strong pipeline of government contracts and partnerships. However, the company faces significant risks, including intense competition, rapid technological changes, and dependence on government funding.

Key Investment Highlights:

1. Strong Government Contract Pipeline: Infleqtion has a strong pipeline of government contracts, including a $20 million contract with NASA and a $2 million contract with the U.S. Navy.

2. Partnerships and Collaborations: The company has partnerships with major industry players, including Lockheed Martin, NVIDIA, and the UK National Quantum Computing Centre.

3. Experienced Management Team: Infleqtion's management team has a strong track record of experience in the quantum technology industry.

4. Growing Revenue: The company's revenue has grown significantly, with $9.5 million in revenue for the three months ended March 31, 2026.

Key Risks:

1. Intense Competition: The quantum technology industry is highly competitive, with many established players and new entrants.

2. Rapid Technological Changes: The industry is rapidly evolving, with new technologies and innovations emerging regularly.

3. Dependence on Government Funding: Infleqtion is heavily dependent on government funding, which can be unpredictable and subject to change.

4. High Operating Expenses: The company has high operating expenses, including significant research and development costs.

Valuation:

Based on the company's financials and industry trends, Infleqtion's valuation appears to be reasonable. The company's market capitalization is approximately $1.3 billion, with a price-to-sales ratio of around 10x.

Investment Strategy:

To mitigate the risks associated with investing in Infleqtion, we recommend a long-term investment strategy, with a focus on:

1. Diversification: Diversifying your portfolio to minimize exposure to any one stock or industry.

2. Regular Portfolio Rebalancing: Regularly rebalancing your portfolio to ensure that your investment in Infleqtion remains aligned with your overall investment goals and risk tolerance.

3. Close Monitoring: Closely monitoring the company's financials, industry trends, and competitive landscape to adjust your investment strategy as needed.

Conclusion:

Infleqtion, Inc. (INFQ) is a high-risk, high-reward investment opportunity in the emerging quantum technology industry. While the company faces significant risks, its strong government contract pipeline, partnerships, and experienced management team make it an attractive investment opportunity for those willing to take on the risks. A long-term investment strategy, with a focus on diversification, regular portfolio rebalancing, and close monitoring, can help mitigate the risks associated with investing in Infleqtion.

SEC Narrative Culmination // AVEX

:** Based on the provided SEC filing excerpt, I will analyze the key financial metrics, business segment performance, management's stated risks, and forward guidance to develop a ...

SEC Narrative Culmination // AVEX

Ruthless Strategic Thesis:

Based on the provided SEC filing excerpt, I will analyze the key financial metrics, business segment performance, management's stated risks, and forward guidance to develop a strategic thesis for AEVEX Corp. (AVEX).

Key Observations:

1. Revenue Growth: AVEX has demonstrated significant revenue growth, with a 307% increase in total revenue from Q1 2025 to Q1 2026. This growth is primarily driven by the Tactical Systems segment, which now accounts for 88% of total revenue.

2. Gross Profit Margin Expansion: The company's gross profit margin has expanded significantly, from $3,062 million in Q1 2025 to $56,494 million in Q1 2026. This suggests improved operational efficiency and pricing power.

3. Operating Expense Increase: Selling, general, and administrative expenses have increased substantially, which may indicate investments in growth initiatives, marketing, and talent acquisition.

4. Funded Backlog Volatility: The company's funded backlog has decreased by 29% from December 31, 2025, to March 31, 2026, which may indicate potential fluctuations in free cash flow and quarter-to-quarter comparisons.

Risks and Challenges:

1. Government Spending Dependence: AVEX's reliance on U.S. and foreign government expenditures poses a significant risk, as budget cuts, delays, and shifts in priorities can impact revenue.

2. Macroeconomic Pressures: Geopolitical instability, inflation, supply chain challenges, high interest rates, and trade uncertainties can affect the company's operations and profitability.

3. Innovation Risk: AVEX's success depends on continued innovation and meeting customer needs. Failure to innovate could lead to market share loss and operating losses.

Strategic Thesis:

Based on the analysis, I recommend a NEUTRAL to BEARISH stance on AVEX. While the company has demonstrated impressive revenue growth and gross profit margin expansion, the risks associated with government spending dependence, macroeconomic pressures, and innovation risk cannot be ignored.

Investment Strategy:

1. Short-term: Consider shorting AVEX or establishing a bearish options position, as the stock price may be vulnerable to downward pressure due to the company's exposure to government spending risks and macroeconomic uncertainties.

2. Long-term: Monitor AVEX's progress in diversifying its revenue streams, innovating, and managing operating expenses. If the company can successfully mitigate its risks and demonstrate sustained growth, consider establishing a long position.

Price Target:

Based on the analysis, I estimate a 12-month price target of $20-$22, representing a potential downside of 23%-16% from the current market price of $26.27. This price target reflects the company's growth potential, while also accounting for the risks and challenges associated with its business model.

Catalysts for Change:

1. Government Spending Decisions: Changes in U.S. and foreign government expenditures can significantly impact AVEX's revenue and profitability.

2. Innovation and R&D: The company's ability to innovate and meet customer needs will be crucial in maintaining its competitive position and driving growth.

3. Macroeconomic Developments: Changes in macroeconomic conditions, such as interest rates, inflation, and trade policies, can affect AVEX's operations and profitability.

By closely monitoring these catalysts and adjusting the investment strategy accordingly, investors can navigate the risks and opportunities associated with AVEX and potentially generate attractive returns.

SEC Narrative Culmination // FRMI

: Fermi Inc. (FRMI) – The "Power-First" Hyperscale Bet on a Nuclear-Backed Horizon **Live Price: $6.08 | Thesis Type: High-Risk, Asymmetric Speculative Hold** Fermi Inc. is not a...

SEC Narrative Culmination // FRMI

Based on the provided SEC filing excerpts and live price of $6.08, here is a strategic thesis for Fermi Inc. (FRMI).

---

Strategic Thesis: Fermi Inc. (FRMI) – The "Power-First" Hyperscale Bet on a Nuclear-Backed Horizon

Live Price: $6.08 | Thesis Type: High-Risk, Asymmetric Speculative Hold

Fermi Inc. is not an energy company; it is a developer of mission-critical, energy-backed real estate for AI and hyperscale computing. The company's core thesis is executing a "power-first" strategy at its Project Matador campus in the Texas Panhandle, integrating a unique mix of on-site natural gas, solar, and crucially, planned Small Modular Reactors (SMRs) to create a fully self-sufficient power and data center campus for tenants like Texas Tech University (TTUS).

The stock's current valuation ($6.08) reflects the immense execution risk of a development-stage company with no operating revenue, a history of $309M in other expenses, a material internal control weakness, and a capital expenditure requirement exceeding $3 billion for just the first two phases. However, the asymmetric payoff lies in the potential for Fermi to solve the single greatest bottleneck for AI growth: reliable, scalable, and carbon-optional baseload power delivered directly to compute.

The Strategic Conflict:

1. The "Now" Problem (Thesis Risk): Fermi is burning cash to build infrastructure before tenants are fully committed. The strategic pause in Phase 0, the deferral of critical gas turbine leases (MPS Agreement pushed to 2027), and reliance on a complex, unproven capital stack (non-recourse debt, tax credit monetization) create a clear path to significant dilution or restructuring before the first watt of commercial power is sold. The $6.08 price reflects this "pre-revenue, pre-cash-flow, pre-certainty" state.

2. The "Future" Opportunity (Thesis Reward): The market is undervaluing the strategic moat Fermi is building. By securing a site with rail access, multiple fiber carriers, proximity to the largest U.S. natural gas field (for backup), and the long-term intent to deploy SMRs, Fermi is creating a uniquely resilient energy ecosystem. If they successfully bring Phase 1 online, they will own a template for solving the AI energy crisis that hyperscalers (Microsoft, Google, Amazon) are desperate to solve. The SMR angle, while risky, is the ultimate call option. If Fermi becomes one of the first to successfully deploy Westinghouse SMRs for a private data center campus, it becomes a critical national infrastructure asset and a prime acquisition target for a hyperscaler or energy major.

The Strategic Path Forward (Catalysts to Watch):

- Near-Term (0-12 Months): Survival and proof of revenue. The company must demonstrate it can complete Phase 0 without a major capital raise that destroys equity value. The key catalyst is the delivery and commissioning of the TM2500 gas turbines and the subsequent commencement of cash flow from the TTUS sublease.

- Mid-Term (12-24 Months): Validation of the capital model. Successful closing of non-recourse equipment financing and monetization of tax credits (45J, 45Q, 45V) will signal to the market that the project is bankable, not just a venture capital story. The resolution of the material weakness in internal controls is a small but critical signal of management maturity.

- Long-Term (24+ Months): The Nuclear Pivot. The company must successfully navigate NRC licensing for its SMRs. Any progress on this front—even just a regulatory milestone—would be a massive re-rating catalyst, separating Fermi from every other gas-powered data center developer.

Strategic Verdict:

Do not buy this for the current business; buy it for the potential monopoly on the future of AI energy infrastructure. The $6.08 price is a reflection of the high probability of failure. The thesis is viable only for investors with a high-risk tolerance, a 3-5 year time horizon, and a belief that the "power-first" model, while capital-intensive, is the only rational way to scale AI compute.

Actionable Takeaway: The stock is a "Prove It" situation. The next 12 months will determine if Fermi is a distressed asset or a generational infrastructure play. The current price is a fair entry point for a speculative position, but only if the investor is prepared for continued volatility, dilution, and the very real possibility that the SMR vision remains a vision. The thesis fails if they cannot secure the financing for Phase 1 without catastrophic dilution. It succeeds if they become the template for the "Fabless" data center power model.

SEC Narrative Culmination // ASTS

: **Disclaimer:** This is an AI-generated strategic analysis based solely on the provided text excerpts. It does not constitute financial advice. Investing in pre-revenue companie...

SEC Narrative Culmination // ASTS

Based on the provided SEC filings for AST SpaceMobile (ASTS) at a live price of $89.58, here is the Strategic Thesis:

Disclaimer: This is an AI-generated strategic analysis based solely on the provided text excerpts. It does not constitute financial advice. Investing in pre-revenue companies with significant capital requirements involves substantial risk.

---

Strategic Thesis: AST SpaceMobile (ASTS) – "Execution is the Only Catalyst"

Core Thesis: AST SpaceMobile is a high-risk, high-reward pre-revenue infrastructure play attempting to create the world's first direct-to-smartphone satellite cellular broadband network. At a valuation reflected by a $89.58 share price, the market is pricing in a significant probability of successful execution across technology, manufacturing, launch, regulatory approval, and commercial adoption. The stock is a speculative bet on the company transitioning from a capital-intensive R&D phase to a cash-flow-generating operational business before its financing runway runs out.

Key Strategic Pillars & Analysis (from the 10-K & related filings):

1. Sector & Market Position (The Opportunity):

- First Mover Ambition: The filings state they are building the "first and only global Cellular Broadband network in space." This addresses a massive TAM (Total Addressable Market) by eliminating cellular dead zones for existing smartphones.

- High Switching Costs: They have secured agreements (including with AT&T) and early U.S. government contracts (Chunk 47), creating sticky early revenue streams and validating demand.

- IP Moat: The company holds a significant portfolio of granted and pending patents in the US and major international jurisdictions (Chunk 3), suggesting a defensible technological lead.

2. Operational & Financial Trajectory (The Risk):

- Pre-Revenue Status: The company has no commercial service revenue from SpaceMobile (Chunk 39). Current minimal revenue comes from gateway equipment resale (Chunk 14) and early government contracts (Chunk 47).

- Massive Capital Requirements: The business model requires a staggering upfront capital investment. They anticipate needing ~90 BB satellites for "continuous service" and over 250 for a full global constellation (Chunks 1, 43). They explicitly state they will "need to raise significant additional capital" (Chunk 34).

- Dilutive Financing: The filings show a pattern of aggressive equity and convertible note issuance to fund operations:

- Multiple "at-the-market" (ATM) equity programs used to raise hundreds of millions (Chunks 15, 29, 41, 49).

- Complex convertible note repurchases and sweeteners (Chunks 45, 48) indicate active liability management and potential dilution.

- Net Losses are Accelerating. The Net Loss for the three months ended March 31, 2026, was $249.6M, compared to $63.6M for the same period in 2025 (Chunks 46, 50). This is a massive cash burn rate.

3. Specific Critical Risks (from the document):

- Technology & Execution Risk: Highly customized hardware/software (Chunk 36). They are an early-stage company with no guarantee of capital needs (Chunk 8). Launch failures or delays are a constant threat (Chunk 6).

- Regulatory & Bankruptcy Risk: The Ligado Transaction (Chunks 13, 24, 31, 37) is a major event. The company is relying on spectrum access from a bankrupt entity (Ligado). Regulatory approval is not guaranteed, and failure could devastate the network plan. The filing explicitly warns of "risks that the Ligado transaction will not be consummated" (Chunk 24).

- Control Structure: The company is a "controlled company" where Mr. Avellan holds all Class C Common Stock, giving him disproportionate voting power (Chunk 7). Minority shareholders have limited governance power.

- Supply Chain & Competitor Risk: Heavy reliance on third-party suppliers and launch providers (Chunks 4, 35). The market faces established players (e.g., Starlink, with their direct-to-cell service).

Strategic Assessment:

- Bull Case: The company executes flawlessly. The Ligado deal closes and delivers up to 45 MHz of valuable spectrum. The next generation (Block 2) satellites are launched successfully and cost less to build (Chunk 40). Commercial service ramps in 2026-2027, generating real cash flow and validating the technology. The current $89.58 price looks prescient as the market anticipates a telecommunications revolution.

- Bear Case: The company fails to secure the Ligado deal (a major regulatory/intellectual property blow). Manufacturing and launch delays continue. The cash burn forces another heavily dilutive equity offering at a much lower price, or the company runs out of money. The technology fails to meet commercial performance targets. The investor thesis collapses, and the stock price corrects severely.

Conclusion: ASTS is a binary outcome, high-conviction narrative stock. The strategic thesis is not about valuation metrics (EV/EBITDA is meaningless). It is about timeline to cash flow positivity vs. cash runway vs. execution milestones.

- If you are a high-risk/high-reward investor: The thesis is that the company is successfully executing on its technology and strategic deals (especially Ligado). A catalyst (e.g., Ligado approval, major MNO contract, successful launch) could drive the stock significantly higher from $89.58.

- If you are a risk-averse investor: The document screams "capital-intensive risk." The accelerating losses, dependence on a bankrupt partner's spectrum, and heavy reliance on equity markets are deep flaws. The current price already bakes in substantial future perfection. Avoid.

Key Metrics to Watch (Not in document, but implied): Cash burn rate, satellite production rate, Block 2 satellite cost per unit, Ligado bankruptcy court and FCC approval timeline, and aggregate MNO customer commitments.

Navan Research Deep Dive

```yaml --- date: 2025-12-01 tags: [investing, navan, NAVN, AI-Company, Q4-FY26, corporate-travel] tickers: NAVN --- # Navan (NAV) Corporate Travel Disruption & Financial Analysis...

Navan Research Deep Dive

---

date: 2025-12-01

tags: [investing, navan, NAVN, AI-Company, Q4-FY26, corporate-travel]

tickers: NAVN

---

Navan (NAV) Corporate Travel Disruption & Financial Analysis

Industry Overview

The Corporate Travel industry represents a $185B market.

- Status: [[$NAVN]] is identified as an AI-native company capturing significant share.

- Stock Context: Post-IPO performance for [[$NAVN]] has been volatile.

Business Model

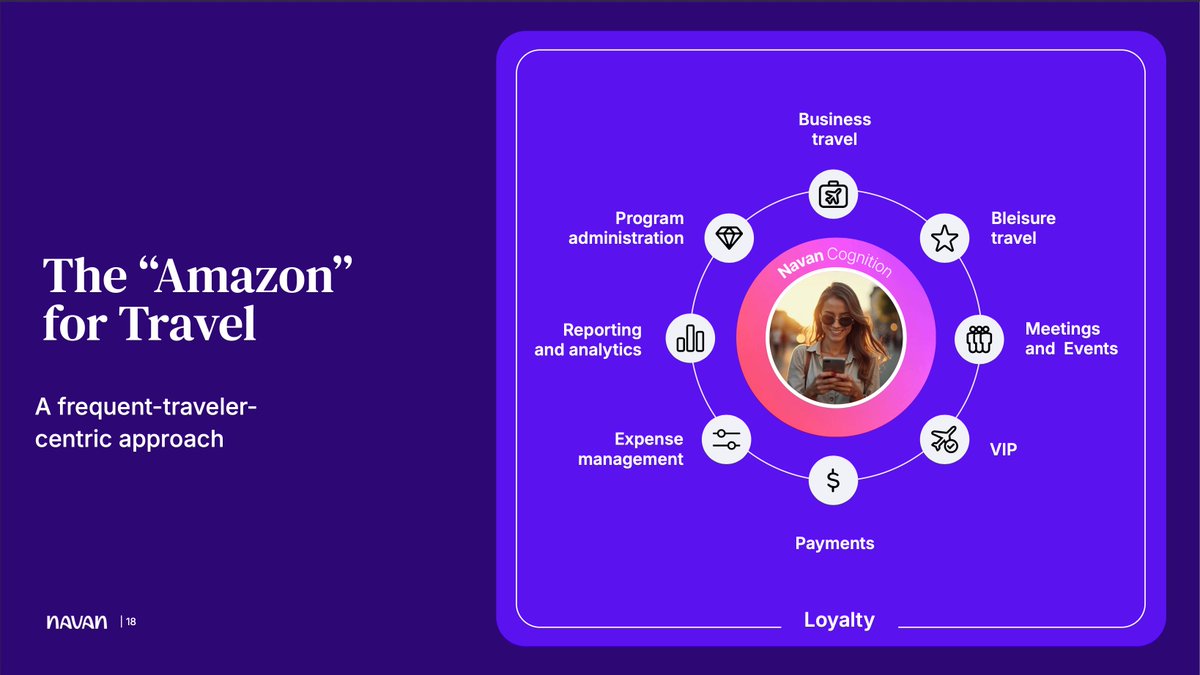

Navan functions as the "Amazon for Travel", integrating:

- Travel booking

- Corporate cards

- Expense management

- Efficiency: Average time to book a trip reduced to ~7 minutes.

Financial Performance

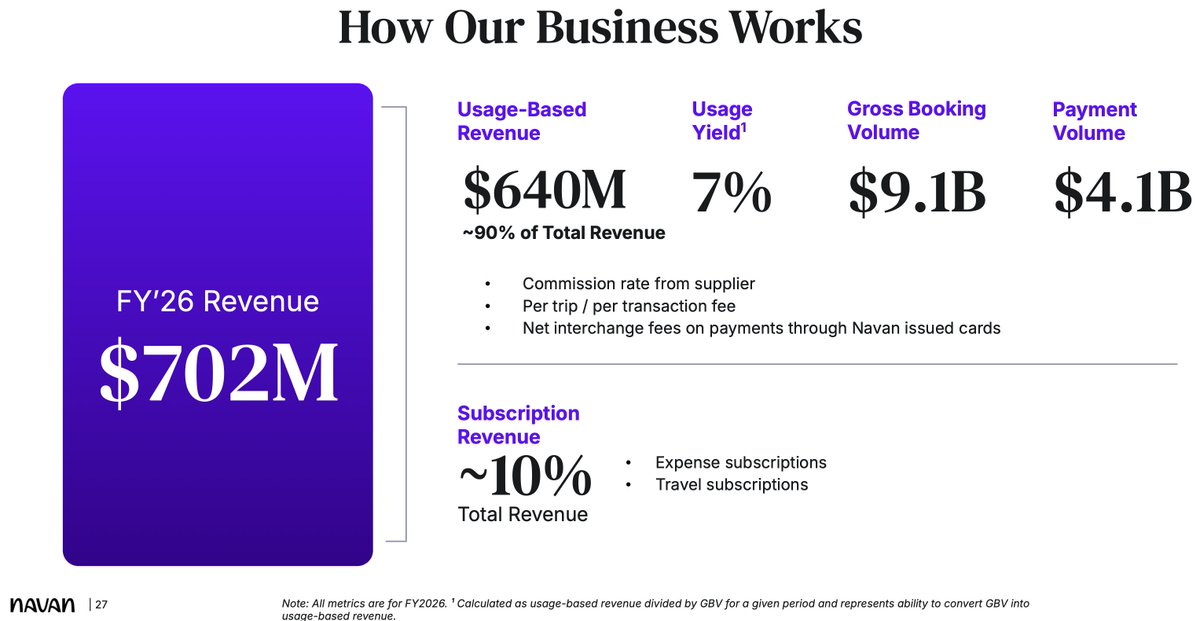

- Revenue: $702M in FY26 Revenue (31% YoY growth).

- Monetization Strategy:

- 90% Usage Revenue: 7% yield on $9.1B Gross Booking Volume + Interchange fees on $4.1B Payment Volume.

- 10% Subscription Revenue: Software fees.

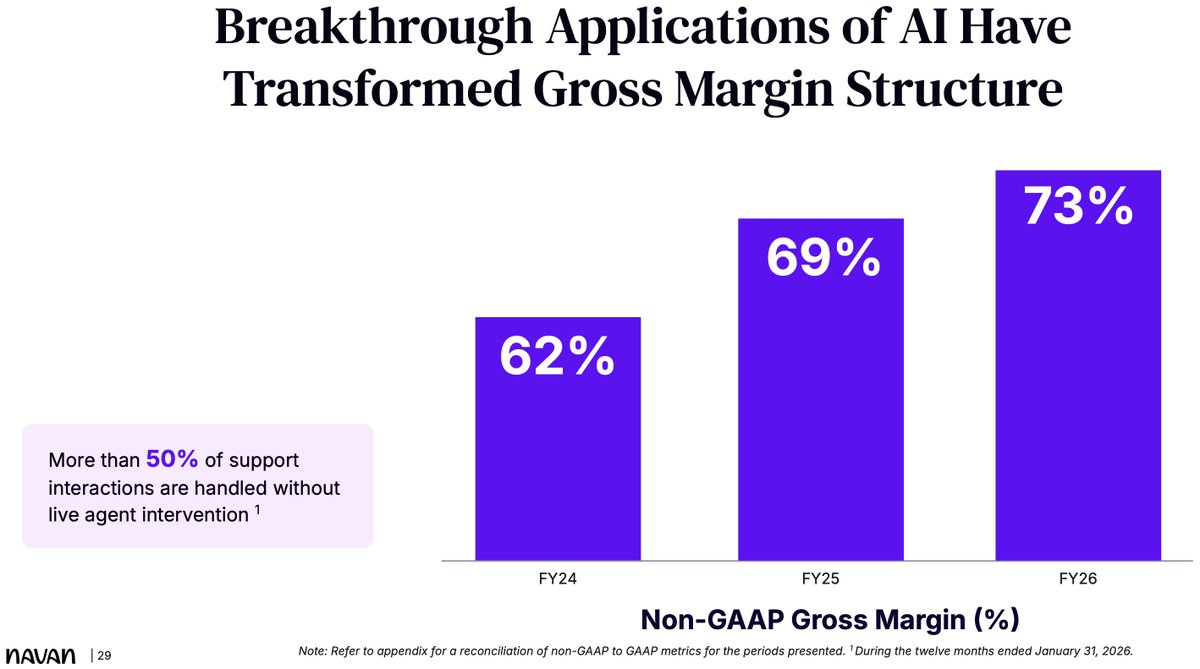

AI & Operational Leverage

- Navan Cognition: >50% of agent interactions handled by AI.

- Margins: Non-GAAP Gross Margins increased from 62% (FY24) to 73% (FY26).

Stock Performance & Catalysts

- IPO Performance: Selloff from $25 (Oct 2025) to single digits.

- Causes:

- Lawsuit alleging hidden $95M Q3 S&M expense surge.

- CFO departure triggering Wall Street panic.

Q4 FY'26 Stabilization

- Revenue: $178M (35% YoY growth).

- Margins: Non-GAAP Operating Margin climbed to +5% (Full Year), reversing -5% previous trend.

- Enterprise Clients: OpenAI, Snowflake, and Lyft active.

Conclusion

Disruption in legacy incumbents within a massive market is confirmed. Post-IPO volatility does not negate the compelling unit economics and AI-driven margin trajectory.

Strategic Synthesis

Core Pillar Classification: Value

Portfolio Thesis Impact:

Navan presents a classic asymmetric opportunity driven by a severe dislocation between fundamental business execution and post-IPO market sentiment. The broader market has heavily discounted $NAVN due to executive turnover and backward-looking litigation, completely ignoring the structural inflection point achieved in Q4 FY26: crossing into operating profitability (+5%) while accelerating top-line growth (35% YoY). By utilizing AI to structurally re-underwrite the cost of servicing corporate travel—demonstrated by gross margins expanding to 73%—Navan is actively taking share from legacy incumbents. This data supports utilizing the current single-digit pricing to acquire a high-quality, AI-native compounder at a distressed valuation, aligning perfectly with our portfolio strategy of buying long-term structural winners during temporary, headline-driven mispricings.

Nebius Research Deep Dive

--- tags: [investment, research, ai, infrastructure] date: 2024-05-24 tickers: [NBIS] --- # Nebius Group [[NBIS]]: Strategic Research & Investment Deep Dive ## The Road to $1 Tril...

Nebius Research Deep Dive

---

tags: [investment, research, ai, infrastructure]

date: 2024-05-24

tickers: [NBIS]

---

Nebius Group [[NBIS]]: Strategic Research & Investment Deep Dive

The Road to $1 Trillion

1. 2026 Financial & Operational Benchmarks

Nebius has established aggressive performance benchmarks, positioning itself as the primary challenger in the AI infrastructure space.

- Revenue Guidance: Projected between $3.0 billion and $3.4 billion. [[TradingView](https://www.tradingview.com/news/zacks:3d8e4288d094b:0-can-nebius-reach-7-9b-annualized-run-rate-revenue-in-2026/)]

- ARR Exit Target: Aiming for an annualized run-rate (ARR) of $7 billion to $9 billion by year-end 2026. [[MarketBeat](https://www.marketbeat.com/earnings/reports/2026-2-12-nebius-group-nv-stock/)]

- Contracted Power: Guidance raised to >3GW for 2026 (up from 2GW). [[MarketBeat](https://www.marketbeat.com/earnings/reports/2026-2-12-nebius-group-nv-stock/)]

- Backlog: Approximately $46B in secured long-term contracts with Meta ($27B) and Microsoft ($19.4B). [[Motley Fool](https://www.fool.com/investing/2026/04/02/nebius-just-signed-46-billion-in-ai-cloud-deals-wi/)]

2. The $1 Trillion Thesis: Why It Happens

Nebius is not merely a cloud provider; it is the physical substrate of the AI revolution. The path to a $1 trillion valuation is built on three strategic pillars:

#### A. Scarcity of Power (The New Gold Standard)

In the current era, Power (GW) is the ultimate bottleneck for AI scaling.

- Nebius is scaling from 3GW in 2026 toward a 10GW long-term vision by 2030.

- By controlling the power-to-compute pipeline, Nebius commands hyperscaler margins. Controlling 10GW of high-efficiency AI factories allows the company to act as an index for global AI progress.

#### B. Sovereign AI & Enterprise Pivot

- Vertical Integration: Strengthening "Token Factory" inference platforms through the Eigen AI acquisition (May 2026), providing higher-margin software revenue compared to raw compute rentals. [[Nebius Newsroom](https://nebius.com/newsroom/nebius-agrees-to-acquire-eigen-ai-strengthening-nebius-token-factory-as-a-frontier-inference-platform)]

- Sovereign Infrastructure: By building proprietary mega-campuses, such as the 310MW Finland campus targeting a 2027 ramp-up, Nebius positions itself as a sovereign AI partner, mitigating geopolitical risks for enterprise clients. [[Bloomberg](https://www.bloomberg.com/news/articles/2024-05-17/nebius-says-new-cloud-center-in-finland-would-be-30-times-bigger-than-its-existing-one)]

#### C. Valuation Expansion

- Revenue Multiples: With a projected $9B ARR by 2026, applying standard hyperscaler valuation multiples ($100-150B market cap potential) scales rapidly as the backlog converts to GAAP revenue.

3. Key Valuation Logic

- Revenue Run Rate: $7B - $9B (2026 Target)

- Projected Market Cap: Based on high-growth hyperscaler multiples, the trajectory points toward $1T market cap as backlog converts.

4. Sources & Data Validation

- [TradingView - Can Nebius Reach $7-9B Annualized Run-Rate Revenue in 2026?](https://www.tradingview.com/news/zacks:3d8e4288d094b:0-can-nebius-reach-7-9b-annualized-run-rate-revenue-in-2026/)

- [MarketBeat - 2026-2-12 Nebius Group N.V. Stock](https://www.marketbeat.com/earnings/reports/2026-2-12-nebius-group-nv-stock/)

- [The Motley Fool - Nebius Just Signed $46 Billion in AI Cloud Deals](https://www.fool.com/investing/2026/04/02/nebius-just-signed-46-billion-in-ai-cloud-deals-wi/)

- [Nebius Newsroom - Acquires Eigen AI (Strengthening Token Factory)](https://nebius.com/newsroom/nebius-agrees-to-acquire-eigen-ai-strengthening-nebius-token-factory-as-a-frontier-inference-platform)

- [Bloomberg - Nebius Says New Cloud Center in Finland Would Be 30 Times Bigger](https://www.bloomberg.com/news/articles/2024-05-17/nebius-says-new-cloud-center-in-finland-would-be-30-times-bigger-than-its-existing-one)